Clients and advisors alike have Long-Term Care on their mind, and the legislative activity coming from the states may be the most effective “marketing” our industry could ask for. The issue is defining an approach advisors can use to guide clients as they evaluate available public options for Long-Term Care.

There is significant change on the horizon in the Care Planning space. The impact of consumers being unprepared for the cost of care and the corresponding stress this places on existing programs and budgets has led many state governments to take action by introducing legislation that creates a “public option” for Long-Term Care insurance. This coming wave of state level Long-Term Care legislation puts clients in a tough position: How to prepare for any new legislation and the associated new income tax while the final form of that legislation remains unknown?

Based on the current state of the most mature LTC legislation from the state of California, a wait and see approach carries a very real risk. As currently written, the legislation may offer an opt out only if consumers have personal Long-Term Care coverage in place prior to the law going into effect. By the time the final details of the legislation are known, however, it could be too late to execute a strategy to allow clients to opt out of the program and avoid any new taxation.

As important as preparing for potential legislation may be, the real risk clients face is not having a care plan in place as they age that includes both how they want to receive care as well as how to pay for it. Many consumers currently feel this risk rather acutely as they care for their own aging parents. Ideally, the potential for new legislation and new taxes will serve as a catalyst for a larger planning conversation that positions clients for any impending legislation as well as maintains forward-looking planning flexibility.

The current state of the California legislation includes five potential designs, each with their own unique attributes. They vary widely in terms of the benefits they could provide as well as the corresponding tax. The most robust design could offer the following benefits:

- LTC Benefits of at least $6,000 per month

- A Benefit Period of two years or longer

- An increasing benefit at a 3% compound rate

There is a view that this level of benefits may represent the minimum standard for personal coverage to qualify for an opt out of the public option and the corresponding tax. Even if this benefit level represents a “safe harbor” of sorts, it is far from an adequate amount of coverage for the typical claim in many markets, both in terms of monthly benefit as well as duration of benefits. This shines a light on the difference between planning for potential legislation and implementing a more comprehensive care planning strategy. Educating clients about the difference may also represent the first step in guiding clients through a decision-making process that addresses both elements of this very real planning challenge. Also, it is critical to consider other designs with longer benefit periods that may be available at similar, if not lower pricing versus looking exclusively at 2-year benefit periods even if only seeking the minimum coverage to qualify for a potential opt-out. One of the primary issues with addressing this challenge is viewing it as a point in time decision.

While it is true clients have a decision to make today that will have downstream consequences, if those consequences are understood in advance, clients can move forward with planning knowing they are prepared for the next steps in the process. At the same time, regardless of the client’s choice today, the end result of a high-quality planning process is the same: Implementation of a plan today, followed by updating their plan once the final form of the legislation is known or at an agreed upon future date.

The next step in the planning process is revisiting the initial decision either upon introduction of new LTC legislation in the client’s state or the currently proposed legislation becoming law. At that point, there are three key questions:

- Is the client eligible for an opt-out?

- If so, should the client pursue an opt out?

- Based on the new legislation and the answer to the prior questions, what changes, if any, should be made to the balance of their existing plan?

These questions are critically important. The second is based on a very healthy question that can be applied to any number of topics: “Just because you can, doesn’t mean you should.” More specifically, until the final form of any legislation is known, it is impossible to predict if opting out is in the client’s best interest, making this the time to make that decision. Next, reviewing these plans periodically, whether based on changes to outside forces like legislation, costs and the like or simple evolution of the client’s view on the issue, is critical to long-term success. Figure 1, Long-Term Care Planning Decision Road Map, outlines a framework for guiding clients through this series of decisions.

Figure 1: Long-Term Care Planning Decision Road Map

In the case of the client who elected to put the safe harbor approach in place, this is likely the time to make their next decision around their funding plan, electing to either rely on the public option or to acquire additional personal coverage to complete their funding plan. This is also an opportunity to review or address for the first time the elements of their care plan beyond funding the cost of care. This includes:

- Creation of any legal documentation that needs to be in place

- Memorializing how the client would prefer to receive care

- Vetting potential providers, facilities and more

Having a truly comprehensive plan in place that addresses all of these elements long before the need for care presents itself increases the quality of the decision-making process and provides the peace of mind that comes with a high level of confidence in the plan.

It’s important to note that while California has been used as an example for this discussion, this same framework can be applied to any of the states currently considering similar legislation and any additional states that may pursue a similar path. Further, there are additional nuances to the California legislation that should also factor into the planning process, and a more comprehensive review of the proposed legislation is highly recommended. Please see Figure 2 for a list of states with current or ending LTC legislation.

Figure 2: States with Current or Pending LTC Legislation

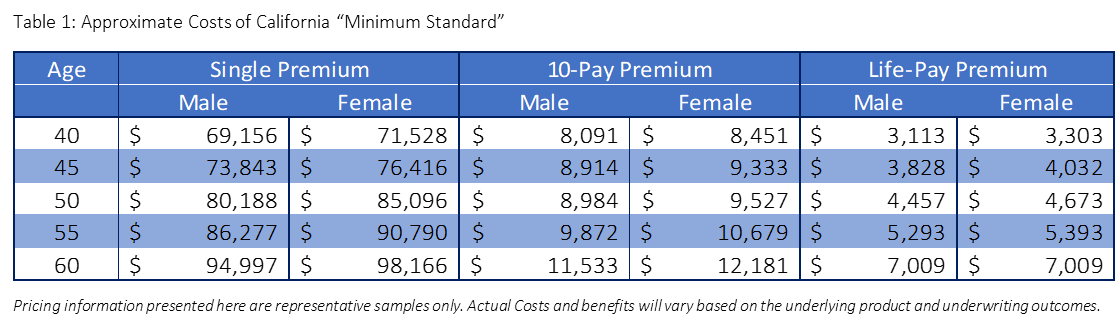

Given the benefit design parameters discussed previously as a potential minimum standard, we can forecast the approximate costs for personal coverage that would meet that standard. These costs are outlined in Table 1, below. This shines a light on the need to evaluate opting out. The economics of these safe harbor designs may require a greater cash outlay than the public option, driving home the need for real planning, not simply tax avoidance.

Table 1: Approximate Costs of California “Minimum Standard”

Pricing information presented here are representative samples only. Actual costs and benefits will vary based on the underlying product and underwriting outcomes.

Most reading this will recall a similar set of circumstances in the state of Washington driven by the Washington Cares Act. The key difference in California and something to keep an eye on in other states, is the timing. Specifically, Washington opened an “opt-out window” after the legislation was enacted that allowed advisors and clients to defer any decisions around pursuing an opt-out. The California proposal does not provide any specificity around a deadline for coverage to be in force to qualify for an opt-out. That said, the earliest effective date referenced in the proposal is January 1, 2024. There is also discussion of a “partial opt-out” for California residents who acquire coverage at a later date. These provisions, like the balance of the specifics relative to the California law, are not finalized.

While not discussed here, it’s important to keep in mind the role life insurance products with Long-Term Care or Chronic Illness riders can play in this process. While these products appear to be less likely to qualify for an opt-out of the California legislation than other products, other states may follow the approach seen in the Washington Cares Act that does not require the COLA provision these products lack. In those instances, it is critical to review the actual language of the legislation in that state for insight around qualifying for an opt-out. Further, if the planning needs of the client indicate that a life insurance policy with a rider is the most appropriate solution, that may supersede qualifying for an opt-out of a public LTC program.

One of the most important lessons from Washington continues to be the impact on product availability. Based on multiple factors to include concerns about persistency and the ability to issue and place policies in a timely fashion, many carriers suspended Long-Term Care sales in the state of Washington well in advance of the deadline for policy placement required for an opt-out. Even with those early deadlines, many carriers struggled to issue policies in a timely fashion based simply on the overwhelming application volumes they received. Given the size of the California market, the possibility of a similar set of circumstances is quite real. The call to action based on all of these factors is to engage clients in an educational and planning process focused on long-term care planning that includes a discussion of any current or potential public options available to them.

Additional reading regarding California Assembly Bill 567:

Please see the following additional resources for more on the proposed California Legislation to include:

{kind=link}

{kind=link}